Time Value of Money | Cfa Level1 Exam | Vibepedia.Network

The time value of money (TVM) is a cornerstone principle in finance. This concept underpins virtually all financial decision-making, from personal savings to…

Contents

Overview

The intellectual roots of the time value of money stretch back centuries, with early thinkers grappling with the concept of interest. While not explicitly termed 'time value of money,' Aristotle, in his work Politics, questioned the morality of usury, suggesting that money itself was sterile and could not reproduce. This early debate hints at a nascent understanding that time plays a role in the value of money. Later, medieval scholars like Thomas Aquinas further refined these ideas, distinguishing between the use of money as a medium of exchange and its use as a store of value, acknowledging that compensation (interest) might be justified for the lender's loss of immediate utility. The formalization of TVM as a quantifiable concept gained traction during the Renaissance, particularly with the development of compound interest calculations by mathematicians like Richard Wittenberg and later, the foundational work on annuities by Johan de Witt in the 17th century. These developments laid the groundwork for modern financial mathematics, making TVM a critical component of economic thought.

⚙️ How It Works

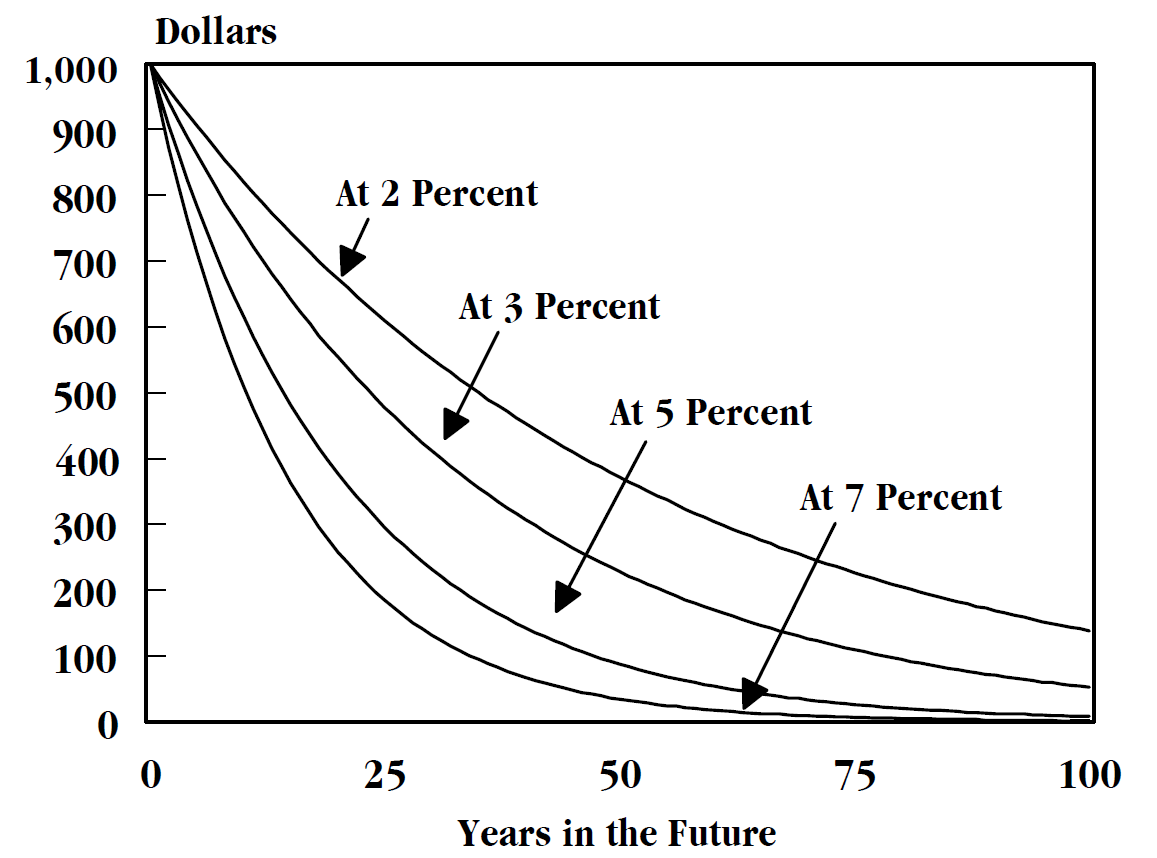

At its heart, the time value of money operates on two fundamental principles: compounding and discounting. Compounding is the process by which an investment grows over time, earning interest on both the principal amount and the accumulated interest from previous periods. Discounting, conversely, is the process of determining the present value of a future sum of money. It answers the question: 'What is a future amount of money worth today?' This is achieved by applying a discount rate, which represents the required rate of return or opportunity cost, to the future cash flow. This mechanism allows for the comparison of cash flows occurring at different points in time, a crucial skill for investment analysis.

📊 Key Facts & Numbers

The quantitative power of TVM is evident in its widespread application. The CFA Level 1 curriculum emphasizes understanding the relationship between present value (PV), future value (FV), interest rate (r), and number of periods (n). Mastery of these variables, including annuities (a series of equal payments over time) and perpetuities (an annuity that continues indefinitely), is essential.

👥 Key People & Organizations

While the concept of TVM is universal, its formalization and application in finance are indebted to numerous economists and mathematicians. Irving Fisher, in his seminal work The Theory of Interest, provided a comprehensive economic framework for understanding interest rates and the time value of money, distinguishing between nominal and real rates. Modern financial theory, heavily reliant on TVM, was advanced by Nobel laureates like Myron Scholes and Robert Merton through their work on option pricing, which inherently involves discounting future payoffs. For CFA candidates, the CFA Institute plays a role in setting the curriculum that dictates the depth and breadth of TVM knowledge required. Textbooks and study providers like Kaplan Schweser and Mark Meldrum play a crucial role in distilling these complex concepts for exam preparation.

🌍 Cultural Impact & Influence

The influence of the time value of money extends far beyond academic finance, permeating everyday financial decisions and societal norms. It's the reason banks offer interest on savings accounts, incentivizing individuals to defer immediate consumption for future gain. Mortgages and car loans are structured around TVM principles, with monthly payments calculated to amortize a loan over a set period, accounting for interest charges. The concept also shapes public policy, influencing decisions on infrastructure projects where the long-term benefits are discounted to present values. Even in personal finance, understanding TVM empowers individuals to make better choices about retirement planning, investment strategies, and debt management, fostering a more financially literate populace. The widespread adoption of financial planning tools and calculators, all built on TVM calculations, attests to its pervasive cultural resonance.

⚡ Current State & Latest Developments

In the current financial landscape, the time value of money remains as critical as ever, though its application is increasingly influenced by technological advancements and evolving economic conditions. The rise of FinTech companies is democratizing access to sophisticated financial tools that leverage TVM for everything from peer-to-peer lending to automated investment management. Central banks' monetary policies, particularly interest rate adjustments by institutions like the Federal Reserve and the European Central Bank, directly impact the discount rates used in TVM calculations, affecting asset valuations and investment decisions globally. Furthermore, the increasing focus on sustainable and ESG investing introduces new dimensions, where long-term environmental and social impacts are factored into financial models, often requiring complex TVM adjustments to quantify future benefits and risks.

🤔 Controversies & Debates

Despite its foundational status, the application and interpretation of TVM are not without debate. A key controversy revolves around the selection of the appropriate discount rate. This rate, representing the opportunity cost of capital, is subjective and can vary significantly based on risk assessment, market conditions, and individual investor preferences. Critics argue that overly optimistic discount rates can justify otherwise poor investments, leading to misallocation of capital. Another point of contention is the treatment of inflation. While standard TVM calculations often use nominal rates, failing to account for inflation can distort the true purchasing power of future sums. The debate intensifies when considering long-term projects or investments in emerging markets, where uncertainty and volatility make discount rate selection particularly challenging and prone to manipulation.

🔮 Future Outlook & Predictions

Looking ahead, the time value of money will continue to be a central tenet of finance, but its application will likely evolve. The increasing sophistication of financial modeling, powered by AI and machine learning, will enable more dynamic and personalized TVM calculations, incorporating a wider array of risk factors and predictive analytics. We may see the development of new frameworks that better account for non-financial factors, such as environmental externalities and social impact, integrating them into the discount rate or cash flow projections. The ongoing digitalization of finance, including the rise of cryptocurrencies and decentralized finance (DeFi), also presents new challenges and opportunities for applying TVM principles in novel contexts, potentially leading to new valuation methodologies and investment strategies that will be crucial for future financial professionals.

💡 Practical Applications

The practical applications of the time value of money are ubiquitous in finance and business. For CFA Level 1 candidates, understanding TVM is essential for: 1. Capital Budgeting: Evaluating the profitability of long-term investments using techniques like Net Present Value (NPV) and Internal Rate of Return (IRR), both of which rely on discounting future cash flows. 2. Bond Valuation: Determining the fair price of a bond by discounting its future coupon payments and principal repayment to their present values. 3. Lease vs. Buy Decisions: Analyzing whether it is more financially advantageous

Key Facts

- Category

- study-materials

- Type

- topic