Market Efficiency | Cfa Level1 Exam | Vibepedia.Network

Market efficiency, primarily embodied by the Efficient-Market Hypothesis (EMH), posits that asset prices fully and instantaneously reflect all available…

Contents

Overview

Market efficiency, primarily embodied by the Efficient-Market Hypothesis (EMH), posits that asset prices fully and instantaneously reflect all available information. This core tenet of modern finance, heavily influenced by the work of Eugene Fama, suggests that consistently outperforming the market on a risk-adjusted basis is impossible because prices only move in response to new, unpredictable information. The theory is crucial for CFA Level 1 candidates as it underpins many valuation and portfolio management concepts, explaining why passive investment strategies like index funds often outperform active management over the long term. Understanding the different forms of market efficiency—weak, semi-strong, and strong—is essential for interpreting market behavior and developing sound investment strategies, even as anomalies challenge its absolute tenets.

🎵 Origins & History

The intellectual lineage of market efficiency stretches back to early 20th-century mathematicians like Louis Bachelier, who drew parallels between stock price movements and Brownian motion. Later, Benoit Mandelbrot further questioned traditional financial models with his work on fractal geometry and market price fluctuations. However, the formalization and widespread academic acceptance of the Efficient-Market Hypothesis (EMH) are largely attributed to Eugene Fama, whose work became a cornerstone of the Chicago School of Economics's approach to finance.

⚙️ How It Works

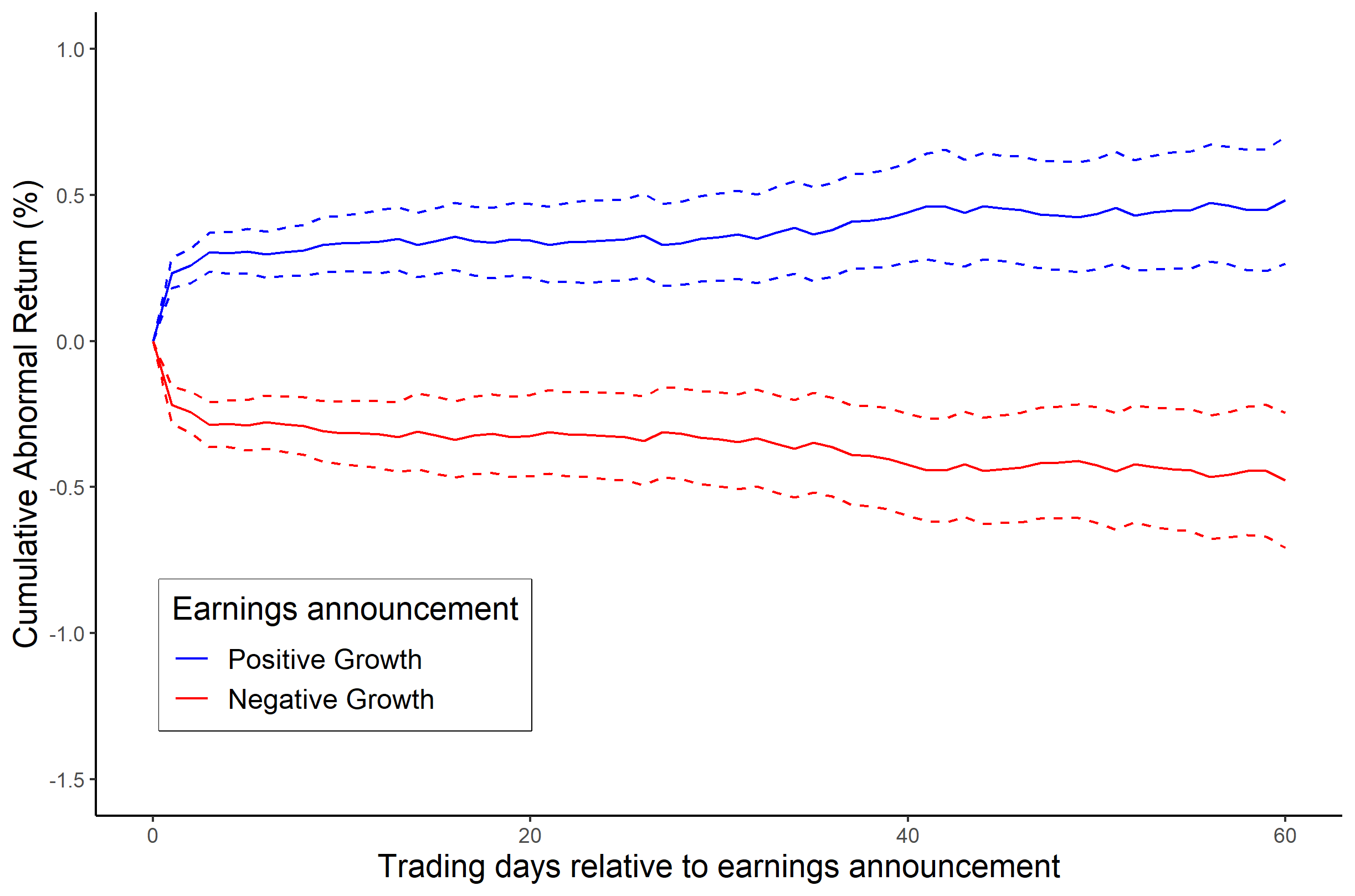

At its heart, market efficiency operates on the principle that in a competitive market, information is rapidly incorporated into asset prices. The EMH is typically broken down into three forms: weak, semi-strong, and strong. Weak-form efficiency suggests that past price and volume data are already reflected in current prices, rendering technical analysis ineffective. Semi-strong form efficiency implies that all publicly available information—including financial statements, news announcements, and economic data—is incorporated into prices, making fundamental analysis based on public data insufficient for consistent outperformance. Strong-form efficiency posits that even private, insider information is reflected in prices, a notion widely considered unrealistic in practice. The core mechanism is the rapid arbitrage activity by informed investors who exploit any mispricing, driving prices toward their 'correct' values.

📊 Key Facts & Numbers

The implications of market efficiency are profound. William Sharpe developed the Capital Asset Pricing Model (CAPM). Studies have shown that a significant majority of mutual funds fail to outperform their benchmark indices over extended periods. This empirical evidence lends considerable weight to the semi-strong form of the EMH.

👥 Key People & Organizations

Eugene Fama is undeniably the central figure, often dubbed the "father of modern finance" for his extensive work on market efficiency and asset pricing. His collaboration with Kenneth French led to the development of the Fama-French three-factor model, which attempts to explain stock returns beyond just market risk, incorporating size and value factors. Other key contributors include Charles Dow, whose early work on stock market averages laid some conceptual groundwork, and Paul Samuelson, who contributed theoretical underpinnings to the random walk hypothesis. Organizations like the CFA Institute incorporate the EMH extensively into its curriculum, recognizing its foundational importance for investment professionals. Academic institutions, particularly the University of Chicago's Booth School of Business, have been hotbeds for EMH research.

🌍 Cultural Impact & Influence

The concept of market efficiency has permeated not just academic finance but also the practical strategies of investment management and regulatory frameworks. It provides the intellectual justification for the rise of passive investing, championed by firms like Vanguard, which offer low-cost ETFs and index funds designed to track market performance rather than beat it. The EMH has also influenced how regulators approach insider trading laws; the strong form of the hypothesis, if fully true, would render insider trading irrelevant, but its illegality stems from the belief that markets are not perfectly strong-form efficient. The cultural narrative around investing often oscillates between the 'get rich quick' schemes promising market domination and the more sober advice that aligns with market efficiency principles.

⚡ Current State & Latest Developments

In the current financial landscape, the debate around market efficiency remains vibrant, often framed by the persistence of market anomalies and the rise of new trading technologies. High-frequency trading (HFT) and algorithmic trading, executed by firms like Citadel LLC and Two Sigma, can incorporate information and execute trades at speeds unimaginable even a decade ago, potentially reinforcing semi-strong efficiency. However, behavioral finance, spearheaded by researchers like Daniel Kahneman and Amos Tversky, continues to highlight psychological biases that lead investors to make irrational decisions, creating deviations from perfect efficiency. The increasing availability of alternative data sources also presents new challenges and opportunities for testing the boundaries of market efficiency.

🤔 Controversies & Debates

The most significant controversy surrounding market efficiency is the existence of persistent market anomalies—patterns or events that seem to contradict the EMH. These include the 'size effect' (small-cap stocks historically outperforming large-cap stocks), the 'value effect' (value stocks outperforming growth stocks), and the 'January effect' (tendency for stock prices to rise in January). Critics, often aligned with behavioral finance, argue these anomalies demonstrate that markets are not always rational. Proponents of the EMH, like Eugene Fama, often counter that these anomalies may be explained by differences in risk that are not captured by standard models, or that they disappear once discovered and exploited. The debate often boils down to whether observed patterns are evidence of market irrationality or simply compensation for unmeasured risks.

🔮 Future Outlook & Predictions

The future of market efficiency will likely be shaped by the ongoing arms race between sophisticated trading technologies and the inherent complexities of human behavior and information dissemination. As artificial intelligence and machine learning become more integrated into trading strategies, the speed at which information is processed will accelerate, potentially pushing markets closer to strong-form efficiency, or at least a highly robust semi-strong form. However, the increasing fragmentation of information sources and the potential for systemic risks, as seen in past crises like the 2008 financial crisis, suggest that perfect efficiency may remain an elusive ideal. The role of regulation in managing information asymmetry and ensuring fair markets will also continue to be a critical factor.

💡 Practical Applications

For CFA Level 1 candidates, understanding market efficiency is not merely academic; it's a practical guide to investment strategy. It explains why a passive approach, such as investing in low-cost index funds, is often recommended for long-term wealth accumulation. It informs the analysis of financial statements, highlighting that while public information is crucial, its impact on price is usually immediate. Candidates learn to differentiate between genuine investment opportunities and noise, recognizing that consistently beating the market requires either superior information (which is illegal if private) or a tolerance for risks that others avoid. This understanding helps in constructing portfolios that align with an investor's risk tolerance and return objectives, rather than chasing illusory alpha.

Key Facts

- Category

- financial-markets

- Type

- topic