Financial Statement Analysis | Cfa Level1 Exam | Vibepedia.Network

Financial statement analysis is the critical process of evaluating a company's financial health and performance by examining its financial statements. This…

Contents

Overview

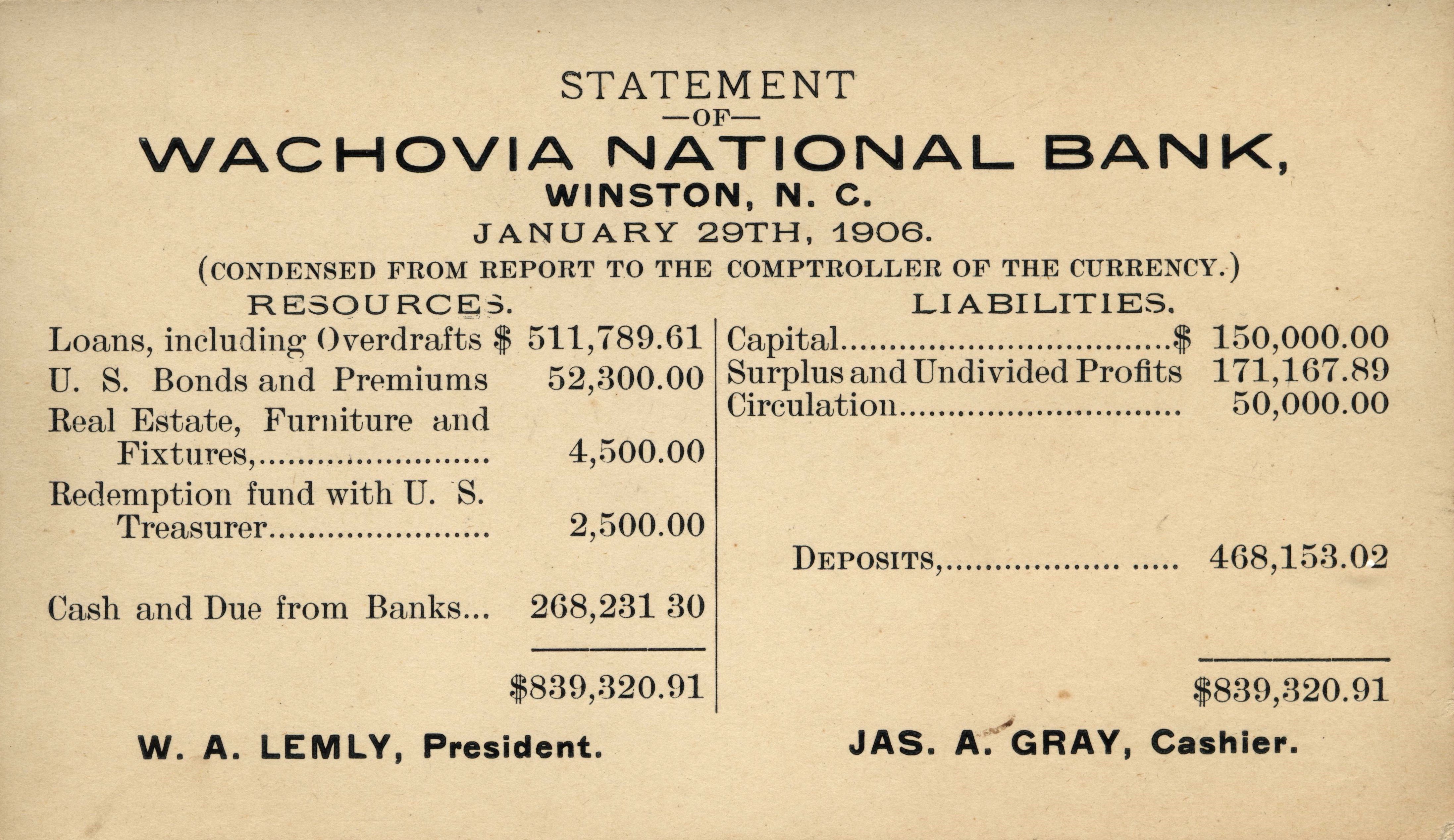

Financial statement analysis is the critical process of evaluating a company's financial health and performance by examining its financial statements. This involves scrutinizing the balance sheet, income statement, cash flow statement, and statement of changes in equity to uncover trends, assess profitability, liquidity, solvency, and operational efficiency. For CFA Level 1 candidates, mastering this skill is paramount, as it forms the bedrock of informed investment decisions and is a heavily tested area. The analysis employs various techniques, including ratio analysis, trend analysis, and common-size analysis, to compare a company against its historical performance and industry peers. Understanding these statements allows investors, creditors, and management to gauge a company's ability to generate earnings, manage debt, and sustain operations, ultimately guiding strategic choices and risk assessment.

🎵 Origins & History

The formalization of financial statement analysis emerged as investors sought to understand the underlying value of businesses beyond mere speculation. Early pioneers like Benjamin Graham and David Dodd, whose seminal work 'Security Analysis' was first published in 1934, laid the groundwork for fundamental analysis, emphasizing the examination of financial statements to identify undervalued securities. The development of accounting standards by bodies such as the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) further refined the information available for analysis, making it more comparable across different entities and jurisdictions.

⚙️ How It Works

Financial statement analysis hinges on dissecting the three primary statements: the balance sheet, which provides a snapshot of assets, liabilities, and equity at a specific point in time; the income statement, detailing revenues, expenses, and profits over a period; and the cash flow statement, tracking the movement of cash from operating, investing, and financing activities. Analysts employ techniques such as ratio analysis—calculating metrics like the current ratio for liquidity or the debt-to-equity ratio for solvency—and trend analysis to observe performance over multiple periods. Common-size analysis, where each line item is expressed as a percentage of a base figure (e.g., total assets or total revenue), is crucial for comparing companies of different sizes or tracking internal changes. The goal is to synthesize this quantitative data into qualitative insights about a company's financial health and future prospects, often aided by management's discussion and analysis (MD&A).

📊 Key Facts & Numbers

Globally, billions of dollars in market capitalization rest on the accuracy of annual financial statements. Ratio analysis is a cornerstone, with over 50 commonly used ratios, categorized into profitability, liquidity, solvency, and efficiency. The CFA Program dedicates significant curriculum to this area, with Level 1 candidates expected to master approximately 70-80% of the core concepts tested.

👥 Key People & Organizations

Key figures in financial statement analysis include academics and practitioners who have shaped its methodologies. Benjamin Graham, often called the 'father of value investing,' pioneered the analytical approach to financial statements. David Dodd, his collaborator, further refined these techniques. More contemporary figures like Warren Buffett exemplify the successful application of these principles, consistently referencing company financial statements in his investment decisions. Organizations such as the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) are instrumental in setting the accounting standards that govern the preparation of these statements, while regulatory bodies like the U.S. Securities and Exchange Commission (SEC) mandate their disclosure for public companies.

🌍 Cultural Impact & Influence

The influence of financial statement analysis extends far beyond Wall Street, permeating business education and corporate strategy globally. It has fostered a culture of transparency and accountability, compelling companies to provide detailed insights into their operations. The widespread adoption of financial modeling software and analytical tools has democratized access to these insights, enabling a broader range of stakeholders, from individual investors to non-profit organizations, to assess financial viability. The very language of business—terms like 'earnings per share,' 'profit margin,' and 'liquidity'—is a direct product of this analytical discipline, shaping how corporate performance is discussed and understood in media and public discourse.

⚡ Current State & Latest Developments

In the current financial landscape (2024-2025), the analysis of financial statements is increasingly incorporating non-financial data, such as Environmental, Social, and Governance (ESG) metrics, to provide a more holistic view of corporate sustainability and risk. The rise of Artificial Intelligence (AI) and machine learning is automating aspects of data extraction and pattern recognition, allowing analysts to process vast datasets more efficiently. Regulatory bodies continue to refine reporting requirements, with ongoing discussions around the adoption of International Financial Reporting Standards (IFRS) in countries like the United States. The focus remains on enhancing comparability and transparency, particularly in complex areas like revenue recognition and intangible asset valuation, as seen in recent updates from the IASB.

🤔 Controversies & Debates

A significant controversy surrounds the potential for 'earnings management'—where companies use accounting flexibility within Generally Accepted Accounting Principles (GAAP) to present a more favorable financial picture than reality. Critics argue that this can mislead investors and obscure underlying operational issues. Another debate centers on the relevance of traditional financial statements in an increasingly digital and service-based economy, where intangible assets often represent a larger portion of value than tangible ones. Furthermore, the comparability of financial statements across different accounting standards (e.g., US GAAP vs. IFRS) remains a persistent challenge, despite convergence efforts by the FASB and IASB.

🔮 Future Outlook & Predictions

The future of financial statement analysis will likely see a deeper integration of big data analytics and AI, moving beyond traditional ratios to predictive modeling. Expect a greater emphasis on real-time financial reporting and the incorporation of non-financial KPIs, such as cybersecurity risk exposure and supply chain resilience, directly into performance assessments. The ongoing push for global accounting standard convergence will continue, aiming to reduce complexity and enhance cross-border comparability. Analysts may also need to develop new frameworks to evaluate companies whose primary value lies in data or network effects, challenging existing valuation models and analytical techniques pioneered by figures like Warren Buffett.

💡 Practical Applications

Financial statement analysis is indispensable for a wide array of practical applications. Investors use it to select stocks for their portfolios, assessing whether a company is undervalued or overvalued. Creditors rely on it to determine a borrower's creditworthiness and ability to repay loans, often focusing on liquidity and solvency ratios. Management employs it for internal performance evaluation, identifying areas for operational improvement and strategic planning. Mergers and acquisitions (M&A) professionals conduct due diligence using this analysis to evaluate potential targets. Even government agencies

Key Facts

- Category

- study-materials

- Type

- topic